Tobias Preis is a Professor of Behavioural Science and Finance at the University of Warwick and a Faculty Fellow of The Alan Turing Institute. Together with his colleague Prof. Suzy Moat, he directs the Data Science Lab at Warwick Business School. His recent research has aimed to analyse and predict real world behaviour with the volumes of data being generated by our interactions with technology, using data from Google, Wikipedia, Flickr and other sources. His research is frequently featured in the news, by outlets including the BBC, the New York Times, the Financial Times, Science, Nature, Time Magazine, New Scientist and the Guardian. He has given a range of public talks including presentations at TEDx events in the UK and in Switzerland.

19 October 2013 | TEDxWarwickSalon:"Can Google predict the stock market?" — "Nearly everything we now do involves interacting with large technological systems, such as the internet. These technological systems generate data trails, or ‘digital traces’, of our day-to-day behaviour. The results I have shown suggest that, in some cases, these traces might make it possible to anticipate our future behaviour."

08 May 2013 | Our new results demonstrate that changes in how often financially related pages were viewed on Wikipedia could have been linked to subsequent movements of the Dow Jones Industrial Average. The study "Quantifying Wikipedia Usage Patterns Before Stock Market Moves" which was co-authored by Helen Susannah Moat, Chester Curme, Adam Avakian, Dror Y. Kenett and H. Eugene Stanley was published in Scientific Reports today.

Supplementary Information is available [ Download ].

25 April 2013 | Our new analysis of changes in Google query volume for search terms related to finance reveals patterns that could be interpreted as early-warning signs of stock market moves. The study "Quantifying Trading Behavior in Financial Markets Using Google Trends" which was co-authored by Helen Susannah Moat and H. Eugene Stanley was published in Scientific Reports today.

Supplementary Information: Search volume data which we retrieved by accessing the Google Trends website in April 2011 [ Download ]. R file which can be used to replicate the results we report [ Download ].

A selected list of media coverage includes:

Financial Times, Google search proves to be new word in stock market prediction. (R. Waters)

Fox Business, Can Google Predict the Stock Market? (Live Interview with M. Francis)

CNN, Can Google search predict stock market? (Live Interview with R. Quest)

BBC Online, Google searches predict market moves. (J. Palmer)

BBC, Can Google predict what the stock market will do? (Interview with D. Gregory-Kumar)

The Telegraph, Google searches can predict stock markets, study finds. (A. Trotman)

Bloomberg Businessweek, 'Big Data' Researchers Turn to Google to Beat the Markets. (B. Warner)

Daily Mail, Can Google predict the stock market? Researchers say analysing search terms can act as 'early warning system'. (M. Prigg)

Nature, Counting Google searches predicts market movements. (P. Ball)

New York Times, Google Search Terms Can Predict Stock Market, Study Finds. (N. Bilton)

Time Magazine, Trouble With Your Investment Portfolio? Google It! (C. Matthews)

The Independent, Hamish McRae: Need a valuable handle on investor sentiment? Google it. (N. Bilton)

CNN, Google can help you time the market. (A. Petroff)

WBS Press Release, Tobias Preis asks: can Google predict the stock market? (A. Potter)

18 October 2012 | Our results show that correlation among the stocks which form the Dow Jones Industrial Average increases at the same rate as market stress. Consequently the diversification effect, which should protect a portfolio, melts away in times of market losses, just when it would be needed most. The study "Quantifying the Behavior of Stock Correlations Under Market Stress" which was co-authored by Dror Y. Kenett, H. Eugene Stanley, Dirk Helbing and Eshel Ben-Jacob was published in Scientific Reports today.

Supplementary Information: Daily closing prices of stocks belonging to the Dow Jones Industrial Average from 1939 until 2010 [ Download ].

WBS Press Release, Dr Tobias Preis's research could lead to the end of stock market crashes. (A. Potter)

05 April 2012 | Our new results demonstrate that Internet users from countries with a higher per capita gross domestic product (GDP) are more likely to search for information about years in the future than years in the past. The study "Quantifying the Advantage of Looking Forward" which was co-authored by Helen Susannah Moat, H. Eugene Stanley and Steven R. Bishop was published in Scientific Reports today.

Supplementary Information: The Future Orientation Index is available for download [ Download ].

A selected list of media coverage includes:

The Guardian, Which countries are the most forward thinking? See it visualised. (A. Sedghi)

New Scientist, Online searches for future linked to economic success. (P. Marks)

Ars Technica, Google Trends reveals clues about the mentality of richer nations. (C. Johnston)

The Verge, Wealthier countries are more interested in the future, Nature finds. (A. Webster)

04 October 2011 | TEDxZurich talk"Bubble Trouble" — When a stock market rises unsustainably, it can create a financial bubble that sooner or later will burst. Dr. Tobias Preis explains whether concepts from physics can be used to create a law describing exactly how such crashes occur.

08 September 2011 | Interview with AsiaEtrading about Switching Processes in Financial Markets, Trading Algorithms using Social Sentiment Data, and Strategies for High Frequency Trading.

07 September 2011 | Interview with the Wall Street Journal — "Researchers Spot Trade Signals In Google Searches" — "Preis, along with Suzy Moat, an academic at University College London, is looking into that now and they hinted that there might be some relevant findings to share with a wider audience soon." (E. Szalay).

11 August 2011 | Interview with the German national weekly newspaper Die Zeit — "Es braucht ein neues Finanzsystem" — "A new financial system is needed." — The two ETH researchers Tobias Preis and Dirk Helbing explain why the world economy is sick, why Adam Smith was wrong - and why we need to think completely differently about money (P. Teuwsen).

12 May 2011 | Physics World Online Lecture Series — "Bubble trouble: how physics can quantify stock-market crashes". Wild fluctuations in the stock prices and currency exchange rates of countries around the globe in the last few years have had a huge impact on the world economy and the personal fortunes of millions of us. Tobias Preis introduces the concept of "econophysics" — The webinar runs for approximately 45 minutes. Moderator: Matin Durrani, editor, Physics World.

10 May 2011 | "We can learn from the large number of tiny bubbles how huge market bubbles emerge and burst. The challenge is to destroy bubbles before they become huge,", concludes Dr. Tobias Preis, researcher at Boston University — Our paper "Switching processes in financial markets" was published in the Proceedings of the National Academy of Sciences.

01 May 2011 | Feature Article "Bubble trouble" published in Physics World — When a stock market rises unsustainably, it can create a financial bubble that sooner or later will burst. Tobias Preis and H. Eugene Stanley examine whether concepts from physics can be used to create a law describing exactly how such crashes occur.

15 November 2010 | "We asked whether or not there is a link between search volume data and financial market fluctuations on a weekly time scale", says lead researcher Dr. Tobias Preis of the Johannes Gutenberg University in Mainz — Our paper "Complex dynamics of our economic life on different scales: insights from search engine query data" was published in the Philosophical Transactions of the Royal Society A.

A selected list of media coverage includes:

TIME magazine, Study: Are Google Searches Affecting the Stock Market? (C. Mayer)

Science, Can Google Predict the Stock Market? (J. Bohannon)

CNN, Google searches predict stock market moves. (K. Voigt)

30 June 2010 | Election of the Federal President (Germany) — Research project Gridscan.com analyzes (together with D. Reith) general public's interest in the candidates using Wikipedia data. Our results were covered by TV and radio stations as well as by various newspapers:

24 May 2010 | Paper demonstrating that multi-spin Monte Carlo simulations of the 2D Ising model can be accelerated on GPU clusters published in Computer Physics Communications.

Supplementary information: Ising source code is available for download [ Download ].

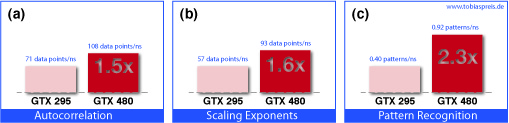

06 May 2010 | CUDA results on new Fermi architecture — GTX 480 benchmark for time series analyses in computational finance. These results were covered by HPCwire.

Benchmark tests use CUDA 3.0 on an Intel i7 920 system. GTX 480 is compared with one chip of the dual chip graphics card GTX 295. Methods are published in T. Preis et al., New Journal of Physics11, 093024, 2009. Results can be obtained up to 200 times faster than on a recent CPU core.

05 January 2010 | Econophysics — Paper (together with H. Eugene Stanley) analyzing trend switching processes in financial markets is published in the Journal of Statistical Physics. Such switching occurs on time scales ranging from macroscopic bubbles persisting for hundreds of days to microscopic bubbles persisting only for a few seconds. We find striking scale-free behavior of the volume and inter-trade times after each switching occurs.

16 September 2009 | Paper demonstrating that the analysis of financial market fluctuations can be accelerated on graphic cards published in the New Journal of Physics. This paper has been selected for inclusion in IOP Select.

Supplementary information: GPU source code is available for download [ Download ].

04 June 2008 | Paper analyzing fluctuation patterns in high-frequency financial asset returns published in Europhysics Letters — Introduction of a new method for quantifying pattern-based complex short-time correlations of a time series. The correlation measure is 1 for a perfectly correlated and 0 for a random walk time series.

FDax | Transaction Prices

FDax | Prices and Volumes

FDax | Prices and Times

Contact Address: — Warwick Business School, University of Warwick, Coventry, CV4 7AL, United Kingdom — Last update on 20 November 2013